The UK’s Department for Transport has published details of its proposed strategy for allocating contracts under the Revenue Certainty Mechanism (RCM), which is intended to give advanced sustainable aviation fuel producers and investors the confidence they need to build and scale first-of-a-kind SAF production plants in the UK. Contracts will be allocated in rounds, with the first, SAF Allocation Round 1 (SAF AR1), open for applications from Q1 2027, shortlisted projects announced from Q4 2027 and contracts awarded from Q4 2028. The proposed size of SAF AR1 will have the aim of supporting up to 230,000 tonnes of annual SAF production capacity. A larger and more technology diverse second round is likely to take place a year after SAF AR1 contracts have been awarded.

Based on a guaranteed strike price model and funded by a levy on aviation fuel suppliers, the RCM should enable UK SAF projects to secure a lower cost of capital, lower the cost of UK SAF production and help projects reach final investment decision (FID), says the DfT in its latest publication on the design of the RCM.

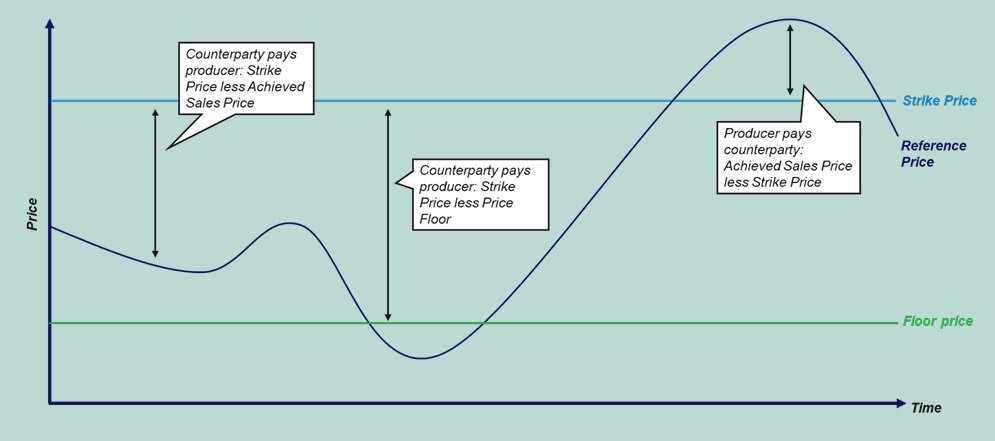

The mechanism involves a private law contract between UK SAF producers and a counterparty – a government-owned entity responsible for administering the RCM and the levy – in which a price is set (the strike price) that a producer will receive for eligible SAF over a fixed period. Where the reference price (the benchmark price against which the strike price is compared) exceeds the strike price, the producer pays the difference to the counterparty. Where the reference price is below the strike price, the producer receives a payment for the difference from the counterparty (see below).

Source: Department for Transport

“The government does not see the RCM as a permanent feature of the SAF production landscape but an intervention that is required while the SAF market is nascent and a lack of certainty and clarity exists around the economics of SAF investment for investors,” says the DfT, which expects the scheme to be running into the 2030s. “The RCM is therefore intended to provide support to first-of-a-kind (FOAK) advanced SAF technologies and feedstocks through a time-limited series of allocation rounds.”

Detailed design of SAF AR1 is currently ongoing and application guidance, which will outline the assessment framework, including the criteria, evidence requirements and submissions expectations at each stage, will be issued when the application window opens early next year. Pre-launch engagement sessions to provide initial information to potential applicants are due to start from Q4 2026.

The strategic objectives of the first round are to support non-HEFA projects representing first commercial deployment of their kind and can provide cost-effective and speedy delivery of UK mandate targets.

“Bids will therefore be subject to robust evaluation and due diligence processes, undertaken with support from the delivery partner for the first allocation round, to assess the credibility, competitiveness and overall value for money of proposed projects before any funding decisions are made,” says the DfT.

“Projects must deliver demonstrable evidence behind information and commitments provided at the eligibility stage. Rigorous technical, financial and commercial due diligence will be carried out on shortlisted projects to verify producer assumptions, proposed schedules and assure deliverability of projects that receive contracts.

“Throughout the development, construction and commissioning phases, the producer will be subject to evidence checkpoints including initial conditions precedent, milestone requirements and operational conditions precedent, which will permit the counterparty to withdraw support if progress stalls and to deter projects submitting speculative bids that are unlikely to meet the commissioning timescales.”

Therefore, it says, RCM support will be initially targeted towards a small number of highly deliverable and mature projects with robust project development fundamentals, while adding the Low Carbon Fuels Fund will still offer grant funding for mature projects and support a development pipeline for less mature projects.

The DfT acknowledges the more of the market that is covered by the RCM, the more distortive the scheme could be on market pricing. “It is important that a market price is established for different forms of non-HEFA SAF as quickly as possible to accelerate projects’ ability to take FID without a RCM contract in the future.”

To estimate the potential levy costs to aviation fuel suppliers, the DfT has considered low and high SAF price scenarios, with low reflecting the lower end of possible SAF market prices (below the strike price) and high reflecting the upper end (above the strike price). For the first allocation round covering 230,000 tonnes per annum over potentially 15 years, under the low scenario the industry would incur levy costs of up to £3 billion ($4bn) and up to £1 billion over 15 years in the high scenario.

“This price discovery mechanism provides an incentive for producers to seek the highest possible price for their fuel, thereby supporting the emergence of a market price for non-HEFA SAF and minimising difference payments from the counterparty to the producer,” explains the DfT.

It says it has “listened carefully” to the concerns of power-to-liquid stakeholders about meeting the UK SAF mandate’s PtL obligation but considers there could be PtL projects competing for SAF AR1 contracts and does not believe ringfenced support for PtL is necessary to ensure technology diversity. However, it says it will reconsider the case for ringfencing as part of the second round, based on how the market has developed to that point.

It is envisioned the second round will support a greater volume of SAF than in SAF AR1 and with a greater focus on portfolio diversity and a “special consideration” for PtL projects.

The DfT reveals that it is considering a transition towards pure price-based mechanisms, for example sealed bid auctions, for future allocation rounds.

“The government will continue to monitor market developments over the course of SAF AR1 and will make a decision on the format of SAF AR2 during the design phase of that round, ensuring sufficient engagement with industry on the matter before taking a decision. All decisions will be subject to value for money and affordability considerations,” it concludes.

Image: Alfanar’s proposed Lighthouse Green Fuels SAF facility in Teesside, UK

Christopher Surgenor

Editor

More News & Features

News Roundup July 2026

High altitude testing of a 100% SAF-powered Gulfstream business jet shows significant non-CO2 benefits

Airbus and MTU form joint venture to develop a fully electric hydrogen fuel cell engine

Deutsche Bank to reduce business travel emissions through SAF deal with Lufthansa Group

News Roundup June 2026

SkyNRG’s latest market outlook finds a SAF industry moving from ambition to implementation