As aviation faces increasing pressure to decarbonise, two carbon pricing systems are now at the centre of the policy debate: the EU’s Emissions Trading System (ETS) and ICAO’s CORSIA carbon offsetting scheme. Today, the ETS applies to all flights operating within the European Economic Area (EEA) as well as departures to the UK and Switzerland. On the other hand, CORSIA is currently a voluntary offsetting scheme set to become mandatory for most ICAO states from 2027. Acknowledging the gap in ETS coverage from not including all international flights departing the EEA, the European Commission is now assessing whether greater action is needed to incentivise decarbonisation beyond Europe. Against this backdrop, Ruchika Kulkarni and Archie Brown of IBA examine which airlines would be the most exposed.

Both systems have a different approach to achieving a common goal of decarbonising the sector. Under the ETS, airlines must monitor their emissions and surrender tradeable emissions allowances to comply, compared to CORSIA where airlines purchase carbon credits from ICAO-approved programmes, and then cancel those credits to meet their emissions obligations.

The EU is considering expanding the scope of the ETS to any flight departing the EEA region, increasing emissions coverage by 109%. We have looked at which routes and airlines would be the most affected, and what are the best likely outcomes for aviation competitiveness and genuine sustainability outcomes.

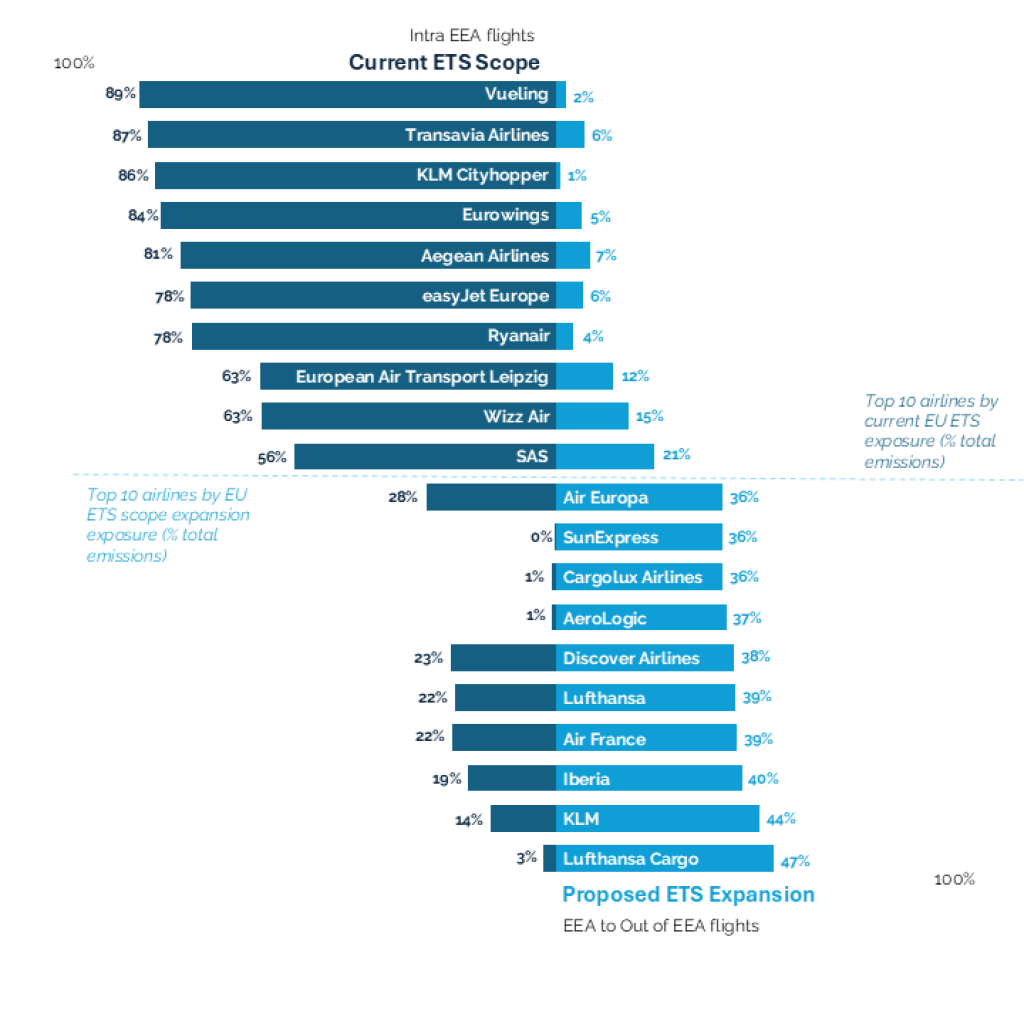

Under the current ETS, aviation exposure is concentrated in intra-European flying, so the airlines most affected today are those with business models centred on short-haul Europe. That is exactly what the chart below shows on the current ETS scope side: the most exposed carriers are overwhelmingly LCCs and regional operators, including Vueling, Transavia Airlines, KLM Cityhopper, Eurowings, Aegean Airlines, easyJet Europe and Ryanair, with 78-89% of their total emissions already covered in several cases. SAS and European Air Transport Leipzig also appear high in the ranking, but there is an obvious pattern. Airlines with dense European networks are already the most exposed because the current regime covers flights within the EEA, as well as departures to the UK and Switzerland.

The proposed expansion side of the chart shows a different set of airlines. Here, the largest step up in coverage shifts towards full-service, long-haul and cargo operators whose emissions currently sit outside the intra-European perimeter. The most affected names include Lufthansa Cargo, KLM, Iberia, Air France, Lufthansa and Discover Airlines, alongside Air Europa, SunExpress, Cargolux Airlines and AeroLogic. In other words, an expansion would not displace the current burden on European short-haul carriers; it would extend that burden to airlines with larger long-haul networks and to cargo operators, many of which currently face much lower ETS exposure as a share of total emissions.

Source: IBA Net Zero

This also helps explain which airlines are more likely to favour expansion. Airlines already heavily exposed under the current system, particularly European LCCs, have the strongest incentive to support a broader scope, since expansion would bring more long-haul traffic into the scheme and narrow the current imbalance. Ryanair has explicitly argued that long-haul flights departing Europe should also fall under ETS, framing it as a matter of competitive fairness.

As an industry, airlines can be sensitive to political and economic shocks that directly affect their operations. In this case, airlines’ position depends largely on their current ETS exposure as a proportion of global emissions and the impact of ETS expansion on their fuel budget.

European low-cost carriers like Ryanair and WizzAir have long supported the idea of expanding the scope of the EU ETS to all international flights departing the EU. Between 78-89% of their global emissions are already exposed to the ETS, and their costs are expected to rise with the discontinuation of free allowances. This disproportionate rise in costs for LCCs then gets passed on to the passenger, which distorts the market and could make low-cost carriers less competitive than airlines who are not currently as exposed. Not expanding the ETS scope can therefore also create the perception that long-haul carriers can “get away” with paying less for their emissions.

Among full-service carriers, airline groups like Air France-KLM and IAG have been vocal about supporting a stronger CORSIA, potentially instead of an ETS expansion. Notably, these are also airlines facing some of the highest additional costs from the expansion of EU ETS, as they operate long-haul flights with higher absolute carbon emissions. Among the top five airlines facing the highest additional costs, KLM faces the highest increase in implied fuel budget at 12%, followed closely by Lufthansa and Air France. Despite being in the top five, Emirates and United Airlines only face a 2-3% increase in the fuel budget owing to their extra-EEA emissions accounting for a small proportion of their overall global emissions.

Both CORSIA and the ETS have their unique advantages. An important positive aspect of CORSIA is that it contributes to development in the global south through its eligible projects, which can otherwise be difficult to finance. The scheme’s eligibility framework also ensures that carbon credits are verified and audited, which is a significant risk with other voluntary development projects. However, current impact is limited: available CORSIA credits today pertain to clean cooking, household energy transition and reforestation projects, which in their current state have a localised and fragmented impact. These projects being relatively small-scale also contributes to CORSIA unit prices being lower and limits the supply of credits.

A significant risk here is that if the scheme cannot raise its ambition and boost the supply of credits for high-impact projects, there might not be enough for airlines to purchase before the mandatory phase, which sets the sector back on its decarbonisation journey.

This is potentially where the EU’s ETS mechanism can be more successful. As a carbon pricing system, it can hold airlines accountable for their emissions from the get-go. Accounting for the 2026 sectoral factor and CORSIA pricing as of April 2026, ETS allowances are priced around 35 times higher than CORSIA.

Some of the revenue collected from the ETS can be re-invested into sustainable transport infrastructure for Europe which also includes the production of alternative fuels. This in turn creates a pathway that benefits aviation’s decarbonisation roadmap despite the initial cost. However, carbon leakage is a risk with ETS expansion (as raised by some full-service airlines), where a strict new policy could incentivise airlines to diversify their hubs to countries with weaker regulation and possibly higher emissions.

Airlines have a vital role to play here. As sustainable aviation fuel (SAF) mandates tighten and environmental compliance gets costlier, more airlines are being vocal about how these compliance mechanisms affect their business models. As it stands, CORSIA is still on track to be mandatory for all member states in 2027, and yet it has not seen widespread uptake of available credits aside from a handful of global commercial carriers. It is in airlines’ own interests to support CORSIA and invest now, to help stimulate demand for credits and generate positive impact. Likewise, ICAO should work alongside its member states and airlines to support the growth of credits supply, and simplify regulation and their release into the market.

The European Commission is expected to publish its impact assessment of CORSIA in July. This will cover an evaluation of the integrity and impact of CORSIA credits, with guidelines on the implementation of CORSIA credits in the EU. This is the most eagerly awaited development in the space, as it can signal a direction on ETS expansion, influence airlines’ behaviour and impact CORSIA’s future in the EU as a credible emissions reduction scheme.

Ruchika Kulkarni is Senior Aviation Analyst and Archie Brown, Senior Analyst – Sustainable Aviation at aviation intelligence and advisory company IBA. A fuller version of this article, with more charts, is available on the IBA website.

Top photo (Fraport): Lufthansa could be one of the most exposed airlines to an extension of the EU ETS

More News & Features

News Roundup July/August 2026

UK aviation group plots route to net zero in updated decarbonisation roadmap

Farnborough Airshow highlights progress on electric and hydrogen propulsion for commercial aviation

Boeing signs MoU with state-owned Pertamina to explore SAF development in Indonesia

Commission proposes a limited extension of the ETS to international departing flights from Europe

Extending the EU ETS to all international flights departing Europe could raise $10bn a year, finds ICCT study